Abstract

To modernise the defence capabilities especially in terms of joint warfighting, the role of semiconductor and an efficient ecosystem is pivotal. Today, India is striving to create a comprehensive semiconductor ecosystem to reduce its reliance on the imported chips. The Indian semiconductor era appears to have begun in 2021 with the launch of the India Semiconductor Mission (ISM). It is anticipated that India is poised to become a dependable supply chain hub by capitalising on the geopolitical unrest amongst the major powers. However, challenges persist involving various factors. To overcome such challenges, India should make collaborative efforts with the major semiconductor hubs of the globe mostly in the Indo-Pacific region. The paper delves into the significance of semiconductors in joint warfighting and how India should strengthen its strategic collaboration with the QUAD countries along with the Southeast Asian nations, Taiwan, Vietnam, Singapore, and South Korea. The paper also discusses various initiatives need to be taken for India to become a global semiconductor hub followed by technological innovation.

Introduction

Modern military technology relies heavily on microelectronics. Semiconductors are an essential part of microelectronic devices, helping to improve functionality and performance. In military applications especially for joint warfighting, semiconductors are of utmost importance due to their ability to process and transmit vast amounts of data quickly and efficiently.1 They enable the development of advanced radar systems, communication devices, navigation systems, and weaponry. Semiconductors also enable miniaturisation, making it possible to create smaller, lightweight military equipment without compromising functionality.2 Overall, semiconductors are indispensable in modern military technology, providing the foundation for advanced and efficient systems that are essential for defence and national security.

Currently, India is aiming to establish a complete ecosystem, from design to manufacturing which would cater to the demands of the country’s defence industry. A number of recent cabinet approvals have opened the door for significant industry advancements. For example, there is an approval for a greenfield initiative in which Tata Electronics Private Limited is collaborating with PowerChip Semiconductor Manufacturing Corporation (PSMC) in Taiwan.3 TATA has also taken the initiative to set up the Outsourced Semiconductor Assembly and Test (OSAT) facility in Morigaon, Assam under the modified scheme for Semiconductor Assembly, Testing, Marking and Packaging (ATMP), with a total investment of about Rs 27,000 crore ($3.29 billion).4

The Odisha state government has encouraged the development of fabless chipmakers and provided them with state-of-the-art electronic design automation (EDA) tools. The Tamil Nadu state government’s semiconductor policy also covers the cost of conducting additional research and development and creating a prototype. Within a decade it is expected that India could become the hub of the global semiconductor ecosystem.5 However, there are several challenges India will have to face. The major semiconductor manufacturing countries are in the Indo-Pacific region. India being a member of the QUAD and a prominent country of the region, have ample of opportunities to collaborate with countries like the US, Japan, Taiwan, South Korea Vietnam, Singapore and Philippines.

The paper makes an effort to understand India’s ecosystem and the challenges it faces due to various factors. It has also elaborated few recommendations as strategies keeping in mind India’s interest to become a global hub in the next ten years.

Role of Semiconductors in Joint Warfighting

There are multiple areas of use of semiconductors. Some of them are covered as under:

- Sensors and Actuators. Wireless sensors, a crucial semiconductor technology product, are one of the essential elements that are becoming more and more important in the military and aerospace industries. By using cutting-edge simulation techniques, sensors contribute to better aircraft control and lightweight design for enhanced weight performance. In addition, the smart sensor is a critical component of the internet of things (IoT) while providing unique identifier for almost anything especially in terms of transmission of data from or about those items over the internet or a comparable sensor network. Actuators are parts that make a system move, and their importance in the aerospace sector has been steadily growing. These actuators are immediately interfaced to flight control and autopilot systems via wireless sensor networks, which initiate the appropriate responses. Thus, a country which is driving into the field of innovation and improvement especially in joint warfighting, will have an increased reliance on the transformative impact of such advanced technologies.

- Microchips It is amazing to see how a micro-chip has the ability to store huge amount of data with the manufacturing of the advanced memory devices. There is an increased interest of usage of non-volatile (NV) memory in autonomous military vehicles due to its data storage even after the cut down of the power supply.7 Recently developed NV chipsets have high physical limits before degradation of the storage layer and can withstand extreme temperatures, similar to military conditions.

- Electro-Optical Systems. Semiconductor technology is becoming important in the development of electrooptical (EO) systems, particularly for military applications. EO/infrared systems have traditionally been used for imaging and situational awareness, particularly in low-light and night circumstances.9 EO is tightly coupled to sensor technology and digital signal processing. Semiconductor is at the heart of signal processing.

- Microcontrollers In recent years, there has been a significant increase in the development of high reliability integrated circuits (also known as microcontrollers). HIREL microcontrollers are being utilised in mega-constellations, which are groups of artificial satellites used for large-scale broadcasting, as well as tiny and picosatellites by governments and private businesses.10

- Logic Devices. A programmable logic device (Pld) is an electrical component used to create reconfigurable digital circuits, such as logic arrays. New logic devices, including field Programmable gate arrays (FPGA), are being developed to meet military requirements.

In the global security scenario while discussing about joint warfighting today, the geopolitics of semiconductors are revolving around the microchips, logic devices, EO, microcontrollers etc. and their production, innovation and control. Thus, a country leading in these technologies will have the leverage to hold a crucial position at a global level.

Understanding the Ecosystem of the Leading Global Semiconductor Hubs and QUAD Partners

Among the leading global semiconductor hubs, the US is the unquestioned global leader in semiconductor design. Six of the top ten global fabless companies by revenue in 201920 were American. The following points show US’s leading percentages in 2018, except in ‘Outsourced ATP’ and ‘Contract Foundries’ where Taiwan was leading:

- Integrated Device Manufacturer (IDMs).S.-based firms account for 51% of total global IDM revenues, followed by firms based in South Korea (28%), Japan (11%), Europe (7%), Taiwan (2%), and Singapore (1%).

- Fabless Firms.S.-based firms account for 62% of total global fabless firm revenues, followed by Taiwan (18%), China (10%), Singapore (7%), Europe (2%), and Japan (1%).

- Contract Foundries. Taiwan-based firms account for 73% of total global contract foundry revenues, followed by firms based in the United States (10%), China (7%), South Korea (6%), Japan (2%), and Singapore (2%).

- Outsourced ATP. Firms based in Taiwan account for 54% of total outsourced ATP revenues, followed by firms based in the United States (17%), China (12%), Singapore (12%), and Japan (5%).

The United States

American corporations dominate two important sub-stages before the design processes: EDA and licenced intellectual property. Chip design is done with EDA software, which has a highly concentrated market due to expensive R&D expenses. Cadence Design Systems, Synopsys, and Mentor Graphics are the three leading players in the space, all based in the United States.16 The first two are American enterprises, while Mentor Graphics was acquired by the German multinational company Siemens in 2017 but continues to operate from the US. In addition to EDA tools, licenced intellectual property is a critical feature of semiconductor design, particularly for CPUs

In 2018, the US-based companies generated 62% of worldwide fabless firm revenues. It is also home to the world’s leading integrated design manufacturers (IDMs), which are companies that build their own chips, such as Intel. In 2018, US-based enterprises accounted for 51% of global IDM revenues.

Japan

While Japan maintained a 50.3% share of the world semiconductor industry in 1988, this percentage has slowly decreased since the 1990s, falling to 10 percent in 2019. Ogino Yosuke, Director of the Device Industry and Semiconductor Strategy office at the Ministry of Economy, Trade and Industry stated:

‘Maintaining and strengthening the domestic semiconductor industry is a crucial strategy for Japan’s future and the safety of its citizens.

In 2021, the Ministry of Economy, Trade, and Industry developed a support strategy for the revival of the semiconductor industry including identifying semiconductor and digital sectors as national priorities. The strategy includes ambitious initiatives, such as the establishment of the Post-5G Fund of JPY200 billion (approximately $1.3 billion) for technological innovation in post-5G and the Green Innovation Fund of JPY2 trillion (approximately $13 billion), which focuses on the development and implementation of semiconductors

In addition, the domestic semiconductor-related sales are expected to exceed JPY15 trillion (about $99.4 billion) by 2030, more than tripling the amount in 2020.

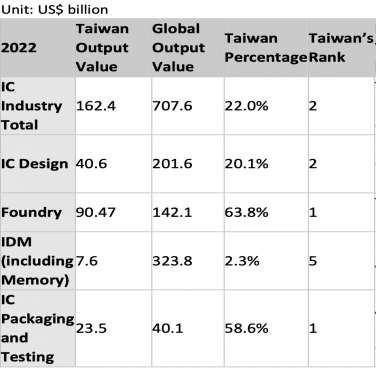

Taiwan

Taiwan produced 63.8 percent of the world’s semiconductors in 2022, with sub-7 nanometer (nm) high-end integrated circuits accounting for more than 70 percent of the global market.23 Taiwan’s integrated circuit (IC) packaging and testing output value is likewise the highest in the worldwide semiconductor market, accounting for 58.6 percent. In addition, Taiwan’s IC design production value accounted for 20.1 percent of the global market, ranking second only to the US. There is no doubt that Taiwan is essential to global economic growth and technological innovation.

More than 90 percent of the primary production sites, as well as cutting-edge technologies, advanced processes, and forward-thinking research and development, remain in Taiwan. Major foreign corporations, including ASML, LAM Research, and Entegris, are expanding their investments in Taiwan, creating production facilities and investing directly in semiconductor companies. Applied Materials and Tokyo Electron have also established training centres for modern process equipment in Taiwan. Leading worldwide ICT and IC businesses, including Apple, Broadcom, and Qualcomm, have chosen Taiwanese companies to provide contract wafer production, IC packaging, and testing services

Table 1 shows the position of Taiwan in various segments of global value chain of semiconductors. Out of the five segments, Taiwan leads in foundry and IC packaging and

Testing. Taiwan holds the second position in terms of IC Industry and IC Design. Taiwan Semiconductor Manufacturing Company Limited (TSMC), the leading Taiwanese semiconductor company, has been invited to establish operations in the US, Japan, and Europe. However, the new plants are not expected to impact Taiwan’s global position in the semiconductor industry.

South Korea

The semiconductor ecosystem is rapidly evolving in South Korea reinforced by investments from both the private and government sectors. Being quite robust in nature, the semiconductor industry in South Korea is able to assert its global competitive edge.

In 2024, the government of South Korea announced a funding package worth 19 billion dollars (26 trillion won) for the chip manufacturing industries. These packages are meant to support research and development, infrastructure including the financial needs. This is also focused to support the medium sized and small enterprises. According to the comments reported by Al Jazeera, President Yoon Suk-yeol stated:

“As you all know, semiconductors are a field of national all-out war.”

The country being home to companies like Samsung and SK Hynix, the top chip manufacturers of the globe, vowed to commence the largest chip centre. This would mostly require investing at least $456 billion. Ensuring supplies of advanced semiconductors has become a critical issue on a global scale, especially with the US and China competing for market dominance. Kim Dae-jong, a professor of business administration at Sejong University in Seoul, told the AFP news agency, “South Korea is supplying 80 percent of the world’s memory semiconductors and has said it is investing 300 trillion won ($220bn) in the Yongin cluster, but there has been a water supply issue with it.” He also added:

“On top of tackling such issues, today’s announcement seems to be an effort to support innovative small and medium-sized enterprises to further strengthen their competitiveness against [rivals] like Taiwan.”

As the ‘China Plus One’ is gaining traction, it has been anticipated that South Korea will gain medium-term business in the semiconductor sector. Dina Ting, Head of Global Index

Portfolio Management at Franklin Templeton affirmed that the US Inflation Reduction Act 2022, which encourages supplies from the free-trade partner might help South Korea in enhancing its business in this sector.

However, Seoul’s semiconductor sector is mostly concentrated in South Korea and China. This definitely enhances the chances of over-reliance on a particular location. To avoid that, diversification of manufacturing is necessary. At this point, South Korea can think of India as an alternative which has shown great enthusiasm in this sector in the last couple of years. India survived the COVID-19 shock demonstrating great resilience along with a stronger political will to expand the semiconductor sector.

International cooperation in this sector is a significant aspect for South Korea today. Developing synergies with other semiconductor hubs of the globe and ensuring supply chain resilience remain critical to its goals. Thus, expanding it to India, it can reduce its dependence just on China and enhance its global presence.

People’s Republic of China (PRC)

PRC has released several directive policy statements that outline a broader framework for science and technology development, which includes China’s semiconductor sector policy. China realised the need to reduce its foreign import since 2009 and remained focused with is initiatives such as the 02 Special Project. According to a 2017 report, at least 16 types of frontend wafer fabrication equipment have been commercialised. Out of the 16, one of the products (7nm process nodes) was approved by the TSMC, the global foundry leader. China started its semiconductor policy to reach the current phase was when it issued the

‘National Integrated Circuit Industry Development Outline’ in 2014 (2014 Outline). The 2014 Outline included development goals for manufacturing tools and materials, as well as for chip design, fabrication, packaging, and testing. The Made in China 2025 (MiC 2025) industry upgrade plan, released by the State Council in 2015, set widely publicised goals of achieving 40 percent and 70 percent self-sufficiency in China’s total IC consumption by 2020 and 2025, respectively.

According to Mercator reports, in 2020, China’s self-sufficiency was just 16 percent in terms of producing ICs. By 2021, the imports increased by 30 percent. This encouraged Beijing to develop an entire ecosystem for IC while commencing in areas where it was lacking. This included R&D capacity, enhancing skilled labourers and extending its collaboration with the global semiconductor hubs.

In the first quarter of 2024, China’s overall output of ICs increased by 40 percent to 98.1 billion units despite the US restrictions on chip making equipment. Trend Force, a Taiwan based IC research company stated:

“The mainland’s global share of mature-process capacity is expected to reach 39 per cent by 2027, up from 31 per cent in 2023.”

By 2025, Beijing expects that its tech sector reaches an annual output worth US $13. 9 billion.

Understanding India’s Semiconductor Ecosystem

In many ways, India’s current focus on Aatmanirbhar Bharat is reminiscent of its early post-independence technology initiatives. Prime Minister (PM) Jawaharlal Nehru’s initial meetings with American industrialists seemed to be similar as that to India’s current industrial plans. During the 1960s, a few Indian companies started manufacturing germanium semiconductors. Fairchild Semiconductors, a leader in integrated circuit (IC) technology, was considering establishing its first Asia facility in India. During this time, Bharat Electronics Ltd. (BEL) and Hindustan Aeronautics Ltd. (HAL), public sector enterprise PSU under the Ministry of Defence were significant players in the Indian semiconductor market. India’s semiconductor sector gained momentum in the 1980s because of the several initiatives undertaken by the then PM Rajiv Gandhi.37

A major initiative was taken in 1984 when the Indian government established Semiconductor Complex Limited (SCL) as a public sector enterprise. Licencing arrangements with Hitachi, AMI, and Rockwell enabled this endeavour. However, within a decade India lost its manufacturing advantage caused by a severe fire that occurred in 1989 at the SCL complex in Chandigarh. The Indian government originally announced the creation of the country’s first semiconductor policy in 2007 although it wasn’t very successful until 2015. However, in 2021-2022, to promote semiconductor factories, ATMPS, and the design ecosystem in India, the Indian government released the ‘Modified Semiconductor Policy’, allocating US $ 10 billion for this purpose.38 In 2023, the US based chipmaker Micron declared that its USD 2.75 billion ATMP would be established in Gujarat, India.39 The Government of India initiated the “India Semiconductor Mission (ISM)” to develop a sustainable semiconductor and display ecosystem as a part of “Program for Development of Semiconductors and Display Manufacturing Ecosystem” in December 2021. The document states that it will be guided by world-class semiconductor and display industry professionals. It will serve as the nodal agency for the efficient and smooth implementation of initiatives for the establishment of semiconductor and display fabs.40 The size of the Indian semiconductor market was estimated at USD 34.3 billion in 2023 and is projected to grow at a CAGR of 20.1 percent to reach USD 100.2 billion by 2032.41 Comparatively, the global projection of semiconductor market was USD 664.54

Billion in 2023 and is projected to reach USD 1.9 trillion by 2032, expanding at a CAGR of 12.5 percent during 2024–2032.42 This illustrates that India’s goals in this sector is aligning with the data projected at a global level. The three factors involving, an expanding market, technological capabilities and the political will definitely put New Delhi in a position to enhance its semiconductor sector.

This data illustrates that India is experiencing significant growth in this sector, aligning well with global trends. The country’s expanding market, coupled with strong political will and technological capabilities, positions it favourably for advancing its semiconductor industry.43

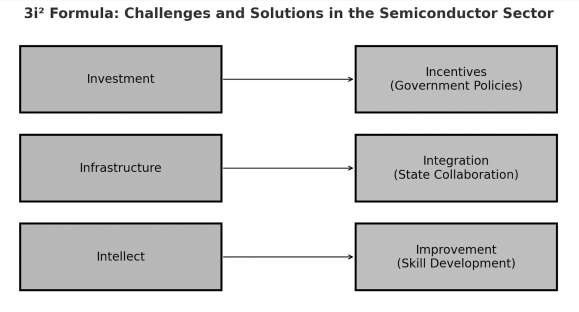

The 3i2 Formula

The 3i2 formula discusses the challenges and solutions/recommendations faced by the semiconductor sector of India. Figure 1 shows the 3i’s investment, infrastructure, and intellect as the major challenges. To deal with these three challenges there are additional 3i’s incentives (government policies), integration (state collaboration), improvement (skill development).

Based on this formula, the challenges and recommendations have been discussed in the following paragraphs.

Challenges for India

Investment

- Setting up a semiconductor manufacturing facility takes a large investment, and India seems quite behind. The technologies used in joint warfare are militaries that use smaller volumes of high-end logic and memory chips and specialised sensors, high efficiency, low power storage devices, quantum computing, AI requiring high-end microprocessors, and GPUs. However, India’s semiconductor ecosystem faces challenges in terms of manufacturing semiconductors required for the high-tech defence technologies. In comparison, India imports a significant amount of semiconductor components. Although the Modi administration has placed a great deal of attention on domestic defence manufacture, there is still a significant reliance on foreign semiconductors. The Defence Public Sector Undertaking (DPSUs) are dependent on the imported semiconductors to a great extent.

- India relies on other nations to meet its needs for semiconductors. From Rs 67,497 crore ($8.23 billion) in 2020–21 to Rs129,703 crore ($ 15.83 billion) in 2022–2023 in chips, imports increased dramatically.44 Meanwhile, China has been attempting to create its own domestic supply chain since 2014, investing tens of billions of dollars annually, but it is still a long way from being able to do so. At least 25 percent of chips are produced domestically by China while importing the remaining ones. Comparatively India still faces challenges in creating a significant indigenous semiconductor ecosystem, as does China.

- PM Narendra Modi has repeatedly stated that India must be ‘Atmanirbhar’ (selfreliant) for it to prosper. However, in terms of the semiconductor sector, this selfreliance would not be that easy because New Delhi does not have much to offer in the semiconductor manufacturing as yet although attempts have been made in the past, nothing much has materialised.46

Infrastructure

- While India has excelled in chip design and electronics manufacture, establishing Semiconductor Wafer Fabrication (FAB) units has proven difficult for several years. Setting up a semiconductor manufacturing facility takes a large investment. It has thus become challenging for India to compete with nearby countries such as China and Vietnam, which have long been preferred locations for global chip manufacturers because to their lower costs. For these reasons, ‘Intel stated’ in 2014 hardly showed any interest in establishing production in India.47

- Another significant challenge is ensuring an uninterrupted power supply. The core issue is that India currently lacks the fundamental infrastructure required to undertake ventures in the chip manufacturing industry. Other global companies, particularly China, are always putting pressure on prices. China is also developing a homegrown chip program with the goal of incorporating local chips into 70 percent of its goods by 2025.48

Intellect

- For decades, India remained a mere observer to the competition in the chip manufacturing industry. Although, the country has a pool of skilled human resources but has not been able to take a lead in fabrication or chip packaging. There is a scarcity of semiconductor engineers who are knowledgeable in device physics and process technologies.

- New Delhi has already started its journey of chip manufacturing with a focus on creating 28 nm node as one of the best alternatives. It is expected that such chips could offer a strategic sweet spot for India’s rapidly developing semiconductor industry. Anurag Awasthi, Vice President of the India Electronics and Semiconductor Association (IESA), stated: “Of this, most applications will be in the aerospace and defence, automotive, industrial, wearables, consumer electronics, and handset segments. We have to cater to our own markets and focus on their growth with the prospective economies of scale and the corresponding job creation”.50 Meanwhile, China’s Semiconductor Manufacturing International Corporation (SMIC), wants to create increasingly tiny 5-nanometer chips by utilising the technology it now has, which is produced in the US and the Netherlands. The HiSilicon unit of Huawei will design the Kirin chips that will be produced on this line.51 Although India has initiated its efforts in terms of design and software but is still at a nascent stage when compared with countries like China, US, Taiwan or South Korea.

Other Challenges for India

- Currently, New Delhi doesn’t have a dedicated policy for this sector to cater to the defence needs of the country. There is a requirement of a ‘comprehensive defence semiconductor policy’. This could be a structural impediment hindering the growth of the indigenous defence manufacturing. In addition, this may also reduce the potential for cooperation between the various branches of the government and the military forces.

- In 2021, at the QUAD summit, the four leaders mentioned about ‘working groups on critical and emerging technologies (C&ET)’. This would mean the four countries would collaborate with each other in strengthening the semiconductor capabilities. However, the question arises as to how far these countries can collaborate being on different trajectories. For example, the US is an equipment, patents, and design leader, in terms of manufacturing Japan is excelling and Australia has a rich reservoir of basic material. Considering, their strengths in the different domains, India has to navigate intelligently to use their potential.

- The semiconductor global value chain is highly integrated and very complex. If merely setting up a semiconductor ecosystem in India will afford India independence from China’s dominance in this sector, it is incorrect. The US-China chip war is an example where both countries are interdependent yet imposing sanctions and trade barriers. Therefore, China’s influence on the Indian semiconductor industry will persist, though India may exercise autonomy in this industry as it develops newer capabilities.

- In light of India’s relationship with Taiwan in this sector, it is crucial to understand the dynamics of the US-Taiwan and Sino-Taiwan relationship too. Taiwan’s collaboration with the US is driven by the former’s leadership in advanced chip manufacturing including initiatives such as CHIPS and Science Act. Furthermore, China remains an important factor, as both Taiwan and the US feel that through technology transfer and investments, they may challenge China’s growth in this field. Comparatively, Taiwan’s relationship with China is strained considering Taiwan’s advancement in this field which poses strategic concern for China. In this context, understanding India’s collaboration with Taiwan is crucial. New Delhi is cautious and doesn’t want to antagonise Beijing. However, aspires to seek benefit from Taipei while attempting to balance its foreign policy. On the other hand, Taiwan saw sense in bolstering its engagement with India given the country’s rising prominence in the Indo-Pacific. In addition, its status as a crucial participant in the QUAD, and the US priority placed on US-India relations couldn’t be ignored. Taiwan has become one of India’s most important economic partners as it develops its semiconductor industry.52 S. Jaishankar, India’s Minister of External Affairs, in November 2023 at the Indian High Commission in London stated: “We have substantial technology and economic and commercial relations with Taiwan and certainly Taiwan has a reputation when it comes to electronics and of course, more recently with semiconductors. So, there has been an upswing in the levels of cooperation.”53 However, New Delhi’s strong interests in attracting investments from the TSMC, have not been fully successful. Such investments were seen as game changer in this sector especially in terms of manufacturing capabilities. Despite such interests from New Delhi, TSMC has not made any plans to invest in greenfield fabrication in India. Instead, the company has concentrated exclusively on the US market. In India, although this is sometimes interpreted as a sign of Taiwan’s lack of dedication and desire, but India needs to develop a favourable business condition, infrastructure and significant demand for the semiconductor market.54 In addition, India has been quite cautious regarding a possible free trade agreement (FTA) with Taiwan. Although Taiwan has been keen to initiate a FTA with India, it did not show much enthusiasm for pursuing such an arrangement. India appears to consider it more as a political agreement than an economic one, and its hesitation may partly be attributed to worries over the trade balance.55 This could be a prudent initiative by New Delhi considering the geopolitical landscape. This might enable India to avoid diplomatic fallout with China and maintain economic ties with Taiwan at the same time.

Recommendations

Incentives

- In 2021, India launched its about $10 billion Production-Linked Incentive (PLI) to promote semiconductor and display manufacturing in the nation. A Design-Linked Initiative (DLI) was also announced to encourage global and domestic investment in design software, intellectual property rights, and other areas.56 However, the application and the approval process for such initiatives should be smoother and quicker devoid of much bureaucratic hurdles.

- Such incentives should be available to more stages of the semiconductor value chain. This could be involving R&D, testing, packaging etc.

- India could emphasis on creating its ‘comprehensive defence semiconductor policy’. The Department of Defence Production in collaboration with the Ministry of External Affairs (MEA) and National Security Council Secretariat (NSCS) could take an initiative in creating a semiconductor strategy. Notably, around 98 percent of semiconductors is used in civilian applications. In order to satisfy the demands of the defence industry, which is looking for high-end, low-volume semiconductors, a sizable subsidy must be provided to the semiconductor sector.

Integration and Collaboration

- With about 800 distinct steps needed, the fabrication of semiconductors is regarded as one of the most complex industrial processes. Three separate processes make up the entire production process: design, fabrication, assembly, and testing. Following fabrication, the chip is put through testing, assembly, and packaging to keep it safe. Some claim that no nation possesses all of the products within its borders.57 Therefore, the four QUAD countries despite being on different trajectories the main objective should be to create enough redundancy in the supply chain to prevent China from dominating or endangering it. The QUAD members must invest in creating a strong collaborative semiconductor ecosystem rather than focusing only on achieving national self-sufficiency in semiconductor production. They can emphasis on the following significant aspects:

- A QUAD consortium needs to be created with the goal of developing a diverse basis for semiconductor manufacturing in these four nations. This would involve pooling resources to advance fabrication capabilities. This strategy will not only save costs, but geographic diversification will strengthen the resilience of the supply chain. From a strategic perspective, fabs built by this cooperation might grant fabless companies in the QUAD grouping priority access.58

- The stated goal of the QUAD semiconductor collaboration should not be to build an exclusive industrial bloc, but rather to serve as a springboard for the formation of broader “bubbles of trust.” The collective strength of QUAD is insufficient to attain total control over the semiconductor industry, nor should it attempt to do so. Rather, the semiconductor QUAD should serve as a foundation for the eventual inclusion of additional siliconpolitik heavyweights like the European Union (EU), Taiwan, Vietnam, South Korea, Israel, and Singapore.59

- Governments are not the best arbiters of efficiency, but the semiconductor companies are. These companies calculated their competitive advantages to optimise costs in their pursuit of efficiency. Global consumers benefited as a result. Governments have recently used export limits and subsidies for domestic semiconductor manufacturing which is going against the trend. Instead of such measures, the QUAD governments should commence more R&D cooperation between countries in terms of knowledge sharing, cross-licensing, cooperative development and licencing agreements.

- One of the reasons India’s world-class semiconductor services industries cannot move into producing its own products is the high cost of EDA tool licences. The QUAD members can offer preferred access to EDA tools at reduced rates by establishing a common finance mechanism, which will diversify fabless design outside of the US.60

- ASEAN countries, namely Taiwan, Vietnam, Singapore, Philippines including South Korea have integrated into the global value chain of semiconductors. Major semiconductor companies have their facilities in these nations. It is a strategic move to collaborate with the ASEAN nations that has potential.61 Collaboration with Taiwan and South Korea is already in progress. India will benefit from Taiwan and South Korea, the semiconductor market leaders. As Taiwan is a leader in the foundry model of the semiconductor manufacture, India can offer skilled technical manpower, stable governance and a large market. In addition, proximity to consumer, proximity to resources play a crucial role. Being closer to resources and the significant markets, India could offer logistical advantage to Taiwan. Today, India is home to roughly 250 Taiwanese businesses. This is sufficient to give India a strong basis for a number of upcoming collaborations. It is noteworthy that the majority of recently established semiconductor manufacturing and assembly/test facilities in India are dispersed over various locations.62

- semiconductor expert stated that the manufacturing chain of semiconductors is diverse, spreading over countries, if not continents. Raw materials, design houses, fabrication units, foundries, assembly and testing and packaging are already located in different countries. By design, no single country can claim total strategic dominance over the entire semiconductor ecosystem. For example, China’s strength lies in small chip manufacturing, logic design and fabs, and Taiwan’s strength in foundries, South Korea’s IDM model, numerous fab plants of Japan, design and fabs of the US, manufacturing machines of Netherlands are intricately dependent on each other for sustenance and profitability. The ecosystem is symbiotic in nature and a collaboration among the semiconductor ‘nations’ is essential. Against this backdrop, the US, Japan, and Australia have a strong case to collaborate with India with their country-specific strengths to ensure a free, open, prosperous Indo-Pacific region. Most importantly, collaboration in the field of semiconductors by the QUAD nations is imperative to tackle the hegemony of China in the Indo-Pacific region.63

- Creation of multiple supply chains should be commenced through multilateralism while picking members from different groupings/alliances. This should enable in keeping the national interest paramount. Such a supply chain will de-risk dependence on a single source and ensure stable and strategic position in the global value chain. notable example is the China Plus One and China Plus Two strategy, and the offset strategy of the US.The third offset strategy which emphasises on leveraging cuttingedge technologies including, artificial intelligence (AI), quantum computing, cyber capabilities etc. In the case of China Plus One and China Plus Two strategies, alternate routes/channels were established outside China to reduce dependence. Apple, FOXCONN and Tesla moving out of China to India is an example of China Plus One. This should be encouraged by New Delhi and be efficient especially in terms of infrastructure, skilled human resource, effective implementation of the government initiatives and building confidence amongst the investors through maintaining consistency in the policies.

Improvement in Skill Development

- Skill upgrade must be a national mission. Use Digital Public Infrastructure to penetrate the skill and knowledge to every district of the nation.

- Encourage academia to establish campuses in the vicinity of the fabs. Universities with R&D facilities must be part of the semiconductor ecosystem. Industry must also invest equally in academic institutions and seek solutions to every problem faced by the industry. For a limited period, the visa may be granted to citizens of the nation’s possessing the required skills as building the skills capability requires a longer time horizon than three to four years.

- In India, ATMP plants have the potential to establish the foundation for the growth of a comprehensive semiconductor ecosystem and could be the focus in the upcoming years. An official in the Ministry of IT stated, “In terms of the semiconductor ecosystem, China holds a 38 percent share of the global market for packaging and India will follow the ATMP path to achieve fab success. The proper method to go is to use this stage as the beginning point because it is a crucial one.”64 Experts in the semiconductor sector think that ATMP facilities not only solve current supply chain issues but also promote an innovative environment. Poornima Shenoy, former president of IESA and presently CEO of Hummingbird Advisors opined, “Setting up an ATMP or OSAT could be the right step. The global market for ATMPs is estimated at $32 billion. It is expected to grow to be worth $180 billion by 2028. There are global ATMP firms registering nearly $12 billion in revenue per year already!”65

Conclusion

India’s semiconductor sector has already been able to draw global interest with investments from various renowned companies. However, New Delhi’s ability to completely capitalise this potential requires emphasis on few aspects including robust design talent especially in terms of manufacturing capacity.

Strengthening collaboration with the QUAD and few Southeast Asian countries is a good initiative, however, India should encourage its cooperation with European countries especially Netherlands which leads the world in the semiconductor industry. The Dutch company ASML is the global leader in the Lithography segment. The government should also play an active role in pushing incentives to attract semiconductor manufacturing in India. The academia especially IIT’s should be encouraged in this sector to bring innovation.

Overall, India has already started its journey and is expected to become acknowledged as one of the world’s leading semiconductor manufacturing nations in due course.

DISCLAIMER

The paper is author’s individual scholastic articulation and does not necessarily reflect the views of CENJOWS. The author certifies that the article is original in content, unpublished and it has not been submitted for publication/ web upload elsewhere and that the facts and figures quoted are duly referenced, as needed and are believed to be correct.

*This paper was originally published in CENJOWS SYNERGY Journal [Vol 3 Issue 2] Aug 2024 Edition.

ENDNOTES

- Mark Stone, “An Overview of Military Semiconductor Applications”, City Labs, [Online: web], Accessed

- 12 June 2024, URL: https://citylabs.net/military-semiconductor-applications/ 2 Ibid

- Sitakanta Mishra and Nisarg Jani, (2024), “The Dawn of India’s Semiconductor Era”, The Diplomat, URL: https://thediplomat.com/2024/03/the-dawn-of-indias-semiconductor-era/

- Press Information Bureau, (2024), “PM to participate in ‘India’s Techade: Chips for Viksit Bharat’ and lay the foundation stone of three semiconductor facilities worth about Rs 1.25 lakh crore on 13th March”,

- Prime Minister’s Office, [Online: web], Accessed 10 July 2024, URL:

- https://pib.gov.in/PressReleasePage.aspx?PRID=2013750#:~:text=The%20Outsourced%20Semiconductor %20Assembly%20and%20Test%20(OSAT)%20facility%20in%20Morigaon,of%20about%20Rs%2027%2C 000%20crore.

- Sitakanta Mishra and Nisarg Jani, (2024), “The Dawn of India’s Semiconductor Era”, The Diplomat, URL: https://thediplomat.com/2024/03/the-dawn-of-indias-semiconductor-era/

- Arjun Gargeyas, (2022), “The Role of Semiconductors in Militray Defence Technology”, Defence and Diplomacy Journal, 11 (22): 45

- Arjun Gargeyas, (2022), “The Role of Semiconductors in Militray Defence Technology”, Defence and Diplomacy Journal, 11 (22): 46

- Arjun Gargeyas, (2022), “The Role of Semiconductors in Militray Defence Technology”, Defence and Diplomacy Journal, 11 (22): 48

- Arjun Gargeyas, (2022), “The Role of Semiconductors in Militray Defence Technology”, Defence and Diplomacy Journal, 11 (22): 49

- Congressional Research Service, (2020), “Semiconductors: U.S. Industry, Global Competition, and

- Federal Policy”, CRS Report, URL: https://fas.org/sgp/crs/misc/R46581.pdf

- Pranay Kotasthane, (2021), “Siliconpolitik: The Case for a QUAD Semiconductor Partnership”, Institute of South Asian Studies, National University of Singapore, [Online: web], Accessed 7 July 2024, URL: https://www.isas.nus.edu.sg/papers/siliconpolitik-the-case-for-a-quad-semiconductor-partnership/

- Naoko Kutty, (2023), “How Japan’s semiconductor industry is leaping into the future”, World

- Economic Forum, [Online: web], Accessed 9 July 2024, URL:

- https://www.weforum.org/agenda/2023/11/how-japan-s-semiconductor-industry-is-leaping-into-thefuture/#:~:text=In%20Japan%2C%20semiconductors%20are%20recognized,domestic%20production%20 system%20of%20semiconductors.

- Chen-Yuan Tung, (2024), “Taiwan and Global Semiconductor Supply Chain”, ROC, Taiwan site, Taiwan

- Representative Office in Singapore, URL: https://www.roc-taiwan.org/uploads/sites/86/2024/02/240202-

- February-Issue.pdf

- Charlotte Trueman, (2024),: “South Korea’s President calls semiconductors a field of ‘all-out war’; announces $19bn support package for industry”, Data Centre Dynamics, [Online: web], Accessed 6 July 2024, URL https://www.datacenterdynamics.com/en/news/south-koreas-president-callssemiconductors-a-field-of-all-out-war-announces-19bn-support-package-for-industry/

- Al Jazeera, (2024), “South Korea unveils record $19bn package to support chip industry”, [Online: web],

- Accessed 6 July 2024, URLhttps://www.aljazeera.com/economy/2024/5/23/south-korea-unveils-record-

- 19bn-package-to-support-chip-industry

- Sayan Ghosh, (2023), “South Korea’s semiconductor ecosystem gets ‘mega cluster’”, Asia Fund Manager, [Online: web], Accessed 10 July 2024, URL: https://asiafundmanagers.com/in/south-koreasemiconductor-ecosystem-gets-mega-cluster/

- John Lee and Jan-Peter Kleinhans, (2021), “Mapping China’s Semiconductor Ecosystem in Global Context”, Mercator Institute for China Studies, URL: https://merics.org/en/report/mapping-chinassemiconductor-ecosystem-global-context-strategic-dimensions-and-conclusions

- Coco Feng, (2024), “China’s semiconductor output jumps 40% in first quarter amid growing dominance in legacy chips”, South China Morning Post, [Online: web], Accessed 12 July 2024, URL:https://www.scmp.com/tech/tech-war/article/3259221/chinas-semiconductor-output-jumps-40first-quarter-amid-growing-dominance-legacy-chips

- Trisha Ray, (2023), “Lessons from India’s past for its semiconductor future”, Observer Research Foundation, [Online: web], Accessed 12 June 2024, URL: https://www.orfonline.org/expertspeak/lessons-from-indias-past-for-its-semiconductor-future

- Ministry of Electronics and Information Technology (2022), “Modified Programme for Semiconductors and Display Fab Ecosystem”, Government of India, URL:

- https://www.meity.gov.in/esdm/Semiconductors–and–Display–Fab–Ecosystem

Dr Ulupi Borah

Dr Ulupi Borah is a Senior Fellow at the Centre for Joint Warfare Studies (CENJOWS). Previously, Dr Borah served as an Assistant Professor at the Rashtriya Raksha University, Gandhinagar. Her expertise lies in the Indo-Pacific region, particularly Japan’s security polices and availed the prestigious JASSO scholarship offered by the Japanese government in 2019. Dr Borah is also researching on Europe and the new security issues, post completion of a course at the Geneva Centre for Security Policy, Switzerland.